The Rally Gets Nervous

Breadth cracked on Wednesday, then most of it healed by Friday. But look closely at what did the healing...

For three weeks I’ve been writing some version of the same happy sentence: the market is broadening, the money is spreading out, more stocks are participating. It was true, and it was good. This week I have to complicate it, because the data did something it hadn’t done in a while.

It got nervous.

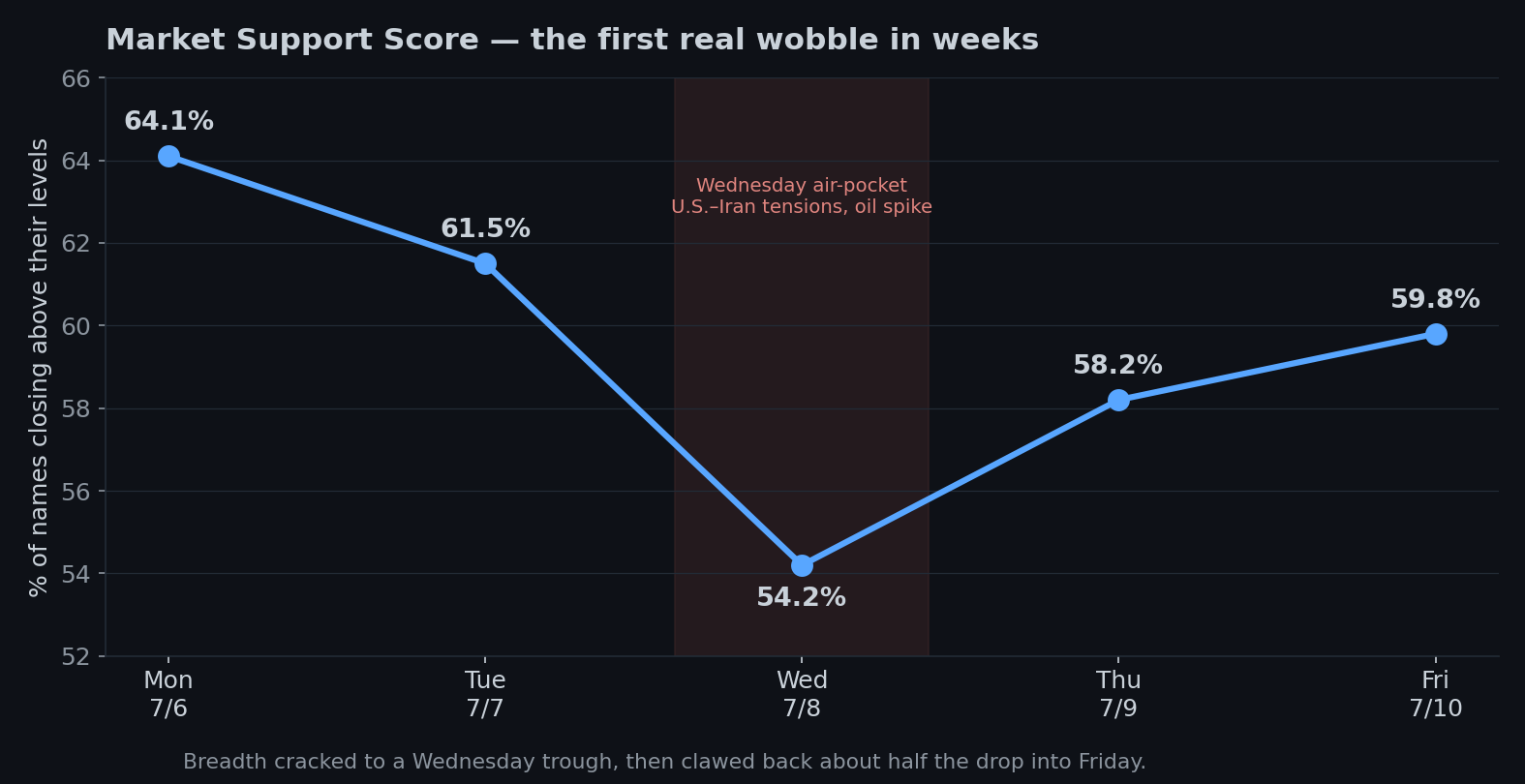

The number cracked, then caught itself

Here’s the share of stocks trading above institutional positioning, day by day: 64.1% Monday, then 61.5%, then a drop to 54.2% Wednesday, then a climb back to 58.2% and 59.8% by Friday. Draw it and you get a V — a real dip mid-week, and a recovery that clawed back about half of it.

That’s the first genuine wobble in this data in nearly a month. For weeks the line only went up. This week it buckled on Wednesday and then found its feet. The market didn’t break. But for the first time in a while, you could see its hands shake.

What spooked it

No mystery here, and for once my data and the entire macro commentariat agree on the cause immediately. The Middle East came back. The U.S.–Iran ceasefire cracked, Iran resumed attacks on shipping in the Strait of Hormuz, the U.S. struck back and revoked oil waivers, and crude jumped about 5% toward $72 a barrel. Oil spiking on war headlines is the oldest risk-off reflex in the book, and Wednesday the reflex fired.

What’s telling is how little it fired. Oil up 5% and a geopolitical flare-up used to be worth a real correction — earlier this year a similar scare helped drive a near-10% drop. This week it bought a one-day dip that was half-recovered by Friday. It seems oil spikes still matter, but the market has grown less sensitive to them — back in March the S&P fell on 10 of 12 days when oil jumped; from April to June it barely flinched. I guess the dog still barks at the mailman. It just doesn’t bite like it used to.

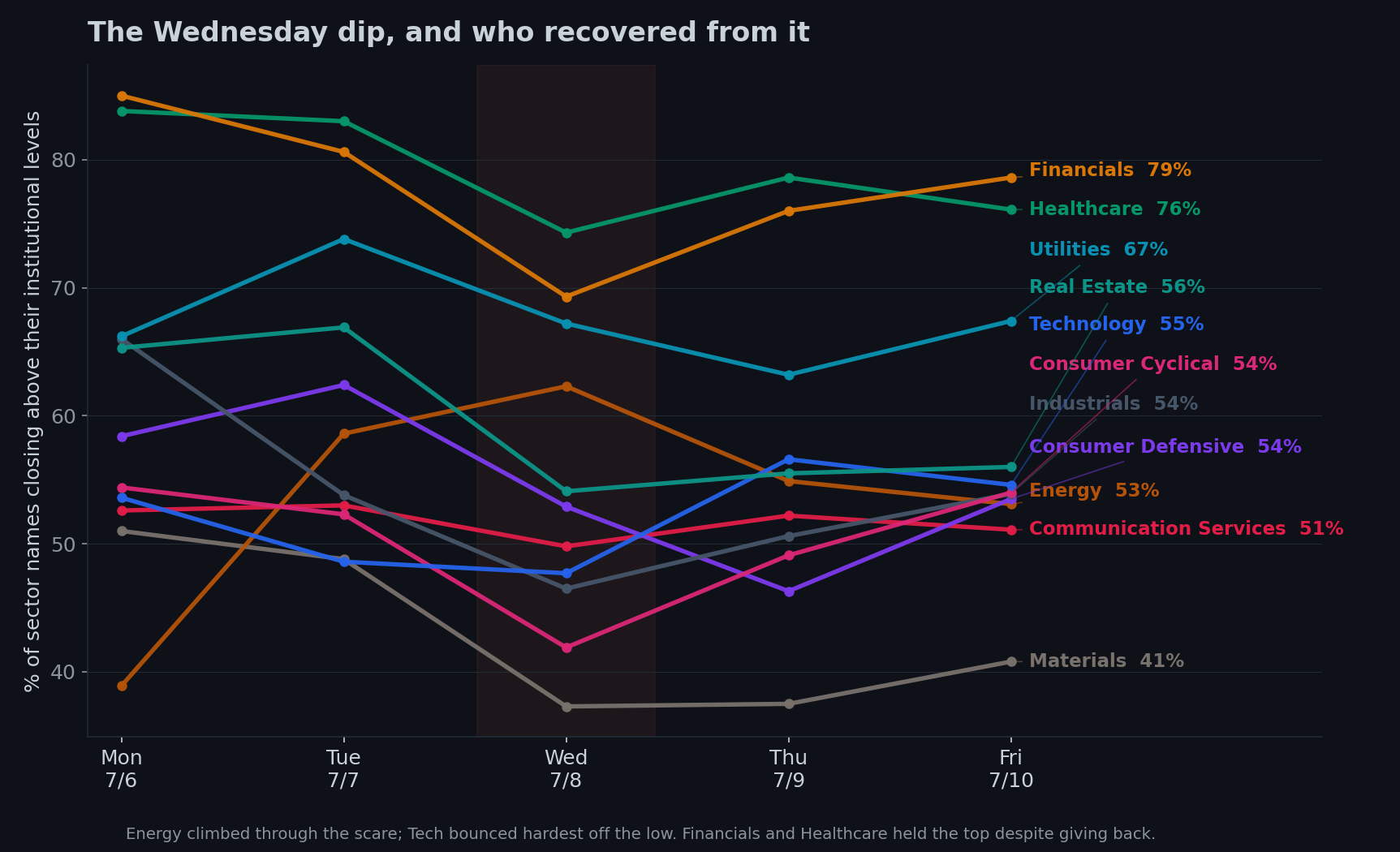

Now look at who did the rescuing

This is the part that matters, and it’s where my data earns its keep.

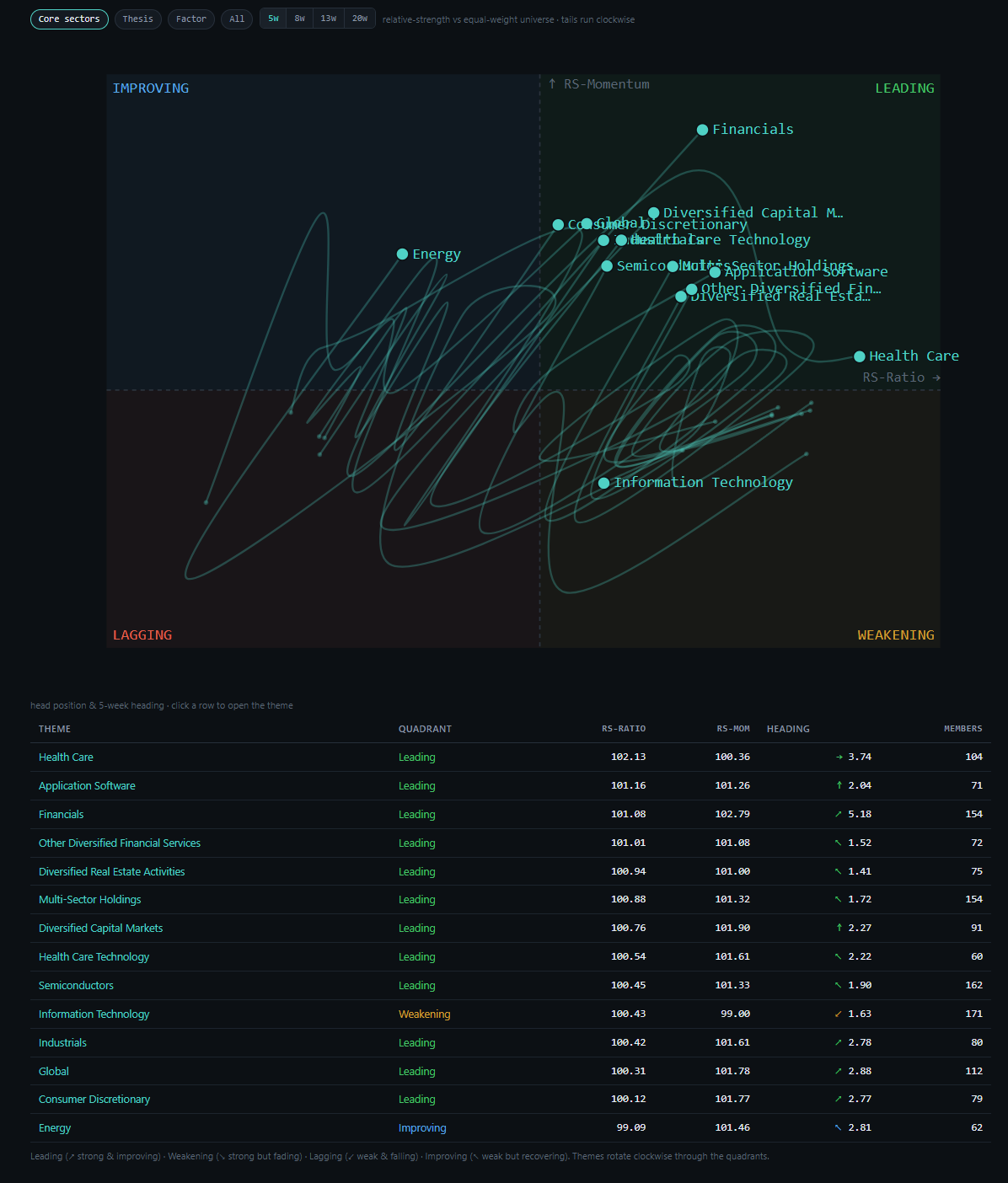

The market recovered on Thursday and Friday. But it did not recover the way it rose the previous two weeks. Those weeks, the gains were broad — hundreds of names across financials, healthcare, industrials, value, international, all climbing together. This week’s bounce was narrow. It was led back by technology and the AI-semiconductor names — the exact crowded trade the money had spent two weeks leaving.

You can see it three ways, and they all agree. In my data, Technology bounced hardest off the Wednesday low — better than any other sector into Friday. In the index tape, the Nasdaq gained 1.74% on the week and growth stocks solidly beat value, while the Dow actually fell half a percent and the small-cap Russell 2000 fell too. A late-week rebound in semiconductor and AI-related shares is what pulled the market out of its hole.

So here’s the shape of the week, honestly stated: the broad market took a hit, and the megacaps carried it back out. That’s a narrower market on Friday than the one we walked in with. Breadth finished the week lower than it started — 60% versus 64% — even though the headline indexes were green. The green came from a handful of the usual giants, not from the thousand names that had been doing the quiet work.

I don’t want to over-read one nervous week. But after three weeks of “the rally is broadening,” the correct update is: this week, under stress, it un-broadened. The crowd’s first instinct when the lights flickered was to run back to the names it knows.

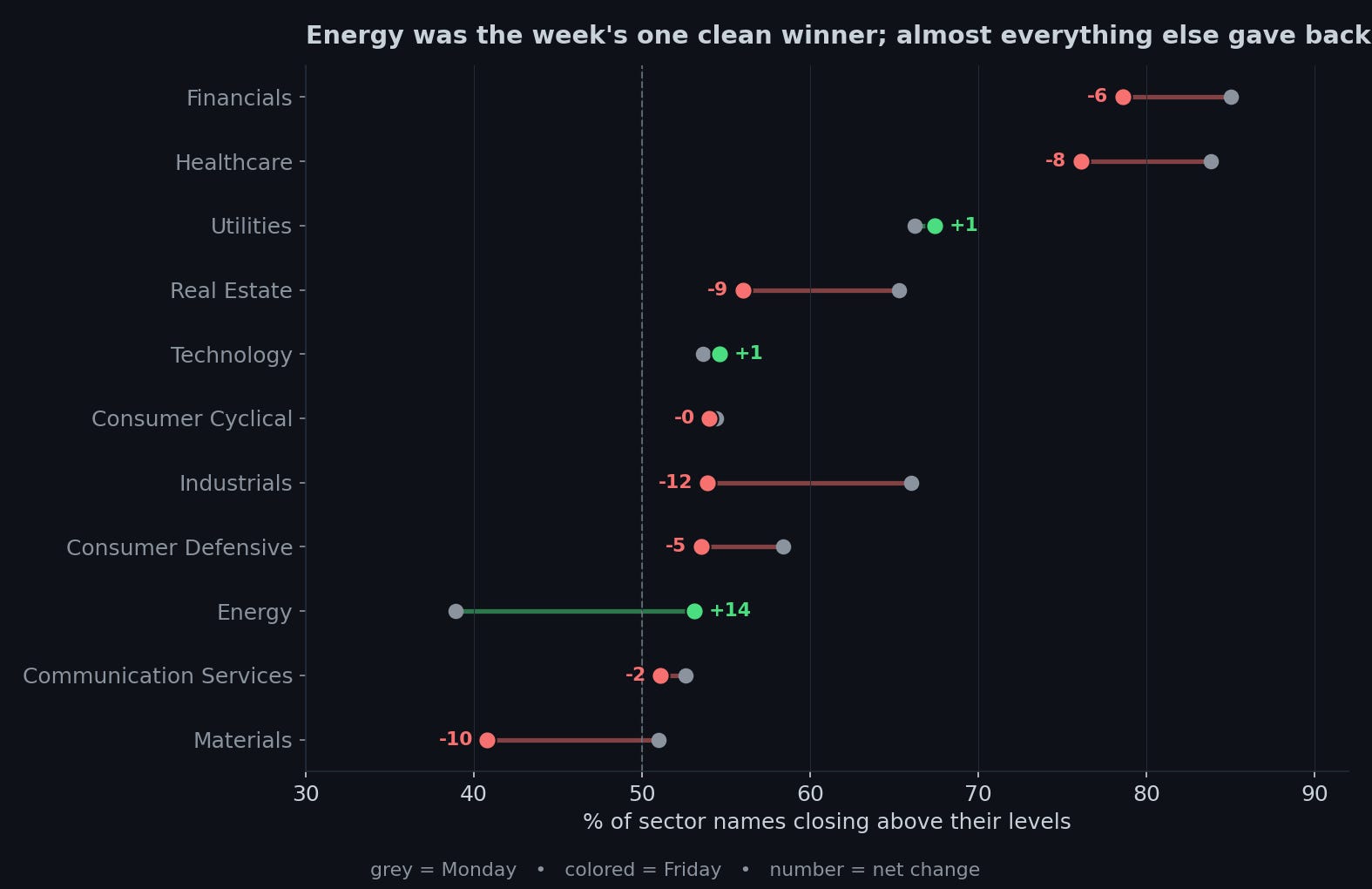

The one clean winner

Almost every sector gave back ground this week. One did the opposite: Energy, up 14 points, the only strong gainer on the board, climbing straight through the scare.

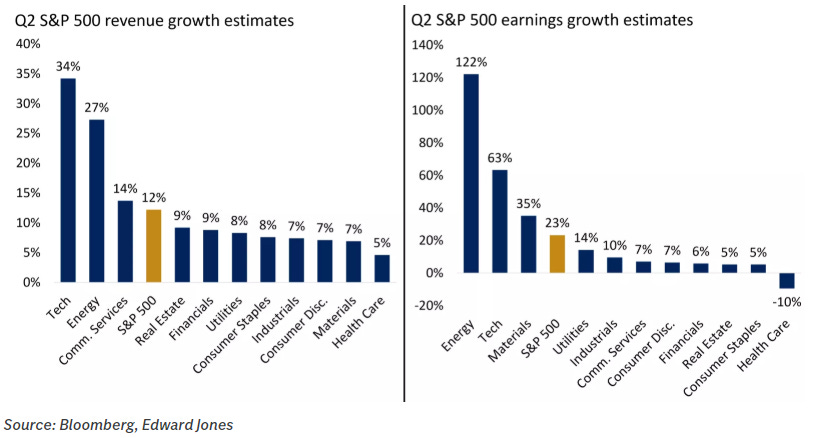

And this one isn’t a puzzle — it’s the resolution of an old one. Two weeks ago I flagged something that bugged me: Energy support had risen while oil fell, and I couldn’t cleanly explain it. This week the relationship snapped back to normal and loud: oil spiked on the war headlines, and Energy stocks went straight up with it. The sector that hates cheap crude loves expensive crude, and this week crude got expensive in a hurry. It helps that Energy is also, quietly, one of the two biggest drivers of this quarter’s corporate earnings growth — so the fundamental and the geopolitical pushed the same direction at once. When the tape hands you a clean cause-and-effect like that, take it; they’re rare.

A quick reminder on how to read the above whisker plot

The leaders held, but one of them is tiring

Financials stayed the strongest sector on my board, right at the top even after giving a little back — and with the big banks kicking off earnings season next week, that’s a leadership perch worth watching. Healthcare, last week’s hero, is a subtler story. It’s still near the top in absolute terms, but it was among the weakest performers this week, and my rotation screen shows its momentum rolling over even as its level stays high — the tell-tale of a leader that’s tiring, not yet falling. Last week Healthcare was the name I told you to notice. This week it’s the name I’d watch to see whether the noticing is over.

The outliers, for their part, were scattered — no single dramatic thread like the Conagra print two weeks ago or the Russell reconstitution before it. The most extreme prints clustered, tellingly, on Wednesday’s dip — when the tape gets violent, the unusual trades pile up — and the recurring names were financials and, once again, a steady drumbeat of international ETFs. That international thread has now persisted for three straight weeks. It’s the quietest story in this data and maybe the most durable.

So: healthy pause, or the party narrowing?

The bullish version: this was a healthy pause. A geopolitical scare hit, the market dipped, quality and AI earnings caught it, and the uptrend resumed. Pauses that refresh are how durable rallies breathe. Earnings season starts next week with the banks, S&P profits are expected up more than 20%, and a strong print re-broadens everything.

The cautious version: this was the broadening ending. For two glorious weeks the market climbed on wide participation; the moment it got scared, it abandoned the broad trade and huddled back into the same seven megacaps that have carried it all year. If that’s the real tell, we’re sliding back toward the narrow, top-heavy market that makes people nervous — a market leaning on a handful of names again.

The thing that settles it is specific and I’ll be watching for it: does the breadth re-broaden, or does tech pull away alone? If next week Financials, Energy, industrials, and the broad middle climb with the megacaps, the pause was healthy and the broadening’s intact. If the indexes grind higher while my support score stays soft — green headlines, weak breadth — then Friday’s narrow bounce was the beginning of re-narrowing, and the prudent move is to stop trusting the index and start watching what’s underneath it. Watch the equal-weight, not the cap-weight. Watch whether the thousand names come back.

What this means, by your clock

If you trade in days to weeks: respect the tape’s resilience — it shook off a real geopolitical scare in two sessions, and the seasonal summer-rally window is still open. But Friday’s bounce was narrow, so don’t confuse green indexes with a healthy market. Trade the leaders that are actually leading (Financials into bank earnings, Energy with the oil bid), keep a hand on the exit given the live geopolitical headline risk, and let the breadth — not the Nasdaq — tell you whether the broadening survives.

If you invest in months to years: one nervous week doesn’t change a durable picture, and the picture is still decent — earnings growing double digits, oil’s grip on stocks loosening, an economy that keeps absorbing shocks. But this week was a small, useful reminder of the market’s central fragility: it is still dangerously dependent on a few enormous names, and the first thing it does when scared is lean on them harder. A portfolio that’s diversified beyond those names isn’t a purity test — it’s insurance against the week the giants finally stumble and there’s nothing broad underneath to catch it.

The through-line, one more time: the headlines said the market fell and then recovered, which is true and nearly useless. The breadth said the recovery was thinner than the fall, carried by the few instead of the many. This week the many got scared and the few did the work. Whether that reverses is the whole question for next week.

Stay steady out there. Wishing you a calm week, the discipline to watch breadth over headlines, and the patience to let the tape prove which story is true before you bet on it.

Thank you for being part of this community and for investing your time in this week’s edition. The quality of this readership — thoughtful, disciplined, engaged — is what makes this work meaningful. I’m grateful to build alongside you. Here’s to a week of clarity, conviction, and well-executed opportunities.

— VolumeLeaders